Exactly How a Secured Credit Card Singapore Can Aid You Reconstruct Your Credit History

Exactly How a Secured Credit Card Singapore Can Aid You Reconstruct Your Credit History

Blog Article

Analyzing the Refine: Exactly How Can Discharged Bankrupts Obtain Credit Cards?

Browsing the realm of charge card applications can be a difficult task, particularly for individuals who have actually been discharged from personal bankruptcy. The process of reconstructing credit history post-bankruptcy postures special obstacles, typically leaving lots of questioning the usefulness of obtaining bank card once more. However, with the ideal strategies and understanding of the eligibility standards, discharged bankrupts can get started on a journey towards monetary healing and access to credit. But just how exactly can they navigate this intricate process and protected debt cards that can aid in their debt reconstructing trip? Allow's check out the methods offered for released bankrupts wanting to restore their creditworthiness with charge card options.

Recognizing Bank Card Qualification Criteria

One vital aspect in bank card qualification post-bankruptcy is the person's credit rating. Lenders often take into consideration credit rating ratings as a measure of an individual's creditworthiness. A higher debt score signals accountable monetary habits and may bring about better charge card alternatives. Additionally, showing a secure earnings and work history can positively affect charge card approval. Lenders look for assurance that the person has the ways to settle any credit report extended to them.

Moreover, people must understand the different sorts of bank card available. Secured charge card, for circumstances, require a money deposit as security, making them much more easily accessible for individuals with a background of insolvency. By comprehending these qualification standards, individuals can navigate the post-bankruptcy credit landscape better and work towards reconstructing their financial standing.

Reconstructing Debt After Bankruptcy

After insolvency, individuals can start the procedure of rebuilding their credit to boost their financial stability. One of the first action in this procedure is to obtain a secured charge card. Protected bank card need a cash down payment as collateral, making them much more accessible to people with a personal bankruptcy background. By utilizing a protected charge card responsibly - making prompt payments and maintaining balances reduced - individuals can demonstrate their credit reliability to prospective lenders.

One more method to restore credit rating after personal bankruptcy is to come to be an authorized user on somebody else's bank card (secured credit card singapore). This allows individuals to piggyback off the key cardholder's positive credit report, potentially improving their own credit rating

Continually making on-time payments for bills and financial debts is essential in restoring credit report. Payment background is a substantial variable in figuring out credit score ratings, so demonstrating liable economic actions is vital. In addition, on a regular basis keeping track of credit report reports for mistakes and inaccuracies can help make certain that the information being reported is right, more aiding in the credit rating restoring process.

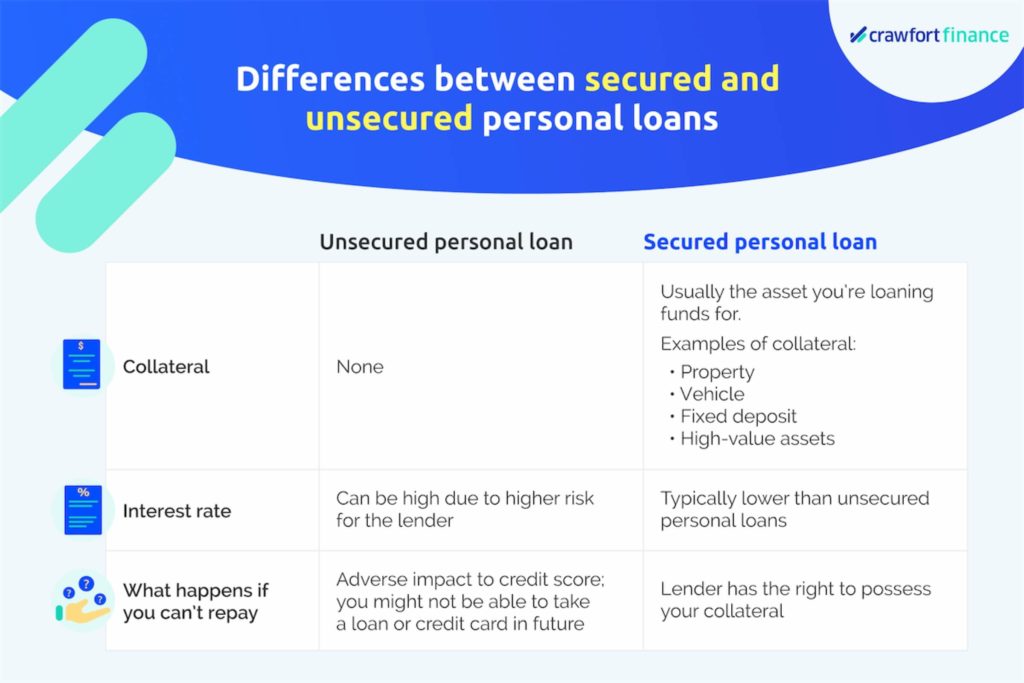

Protected Vs. Unsecured Credit Rating Cards

When considering debt card options, people might encounter the option in between secured and unsecured credit rating cards. Secured credit score cards call for a money down payment as collateral, commonly equal to the credit rating limitation provided. While safeguarded cards supply a course to enhancing credit scores, unsecured cards provide even more adaptability however might be harder to get for those with a struggling credit rating history.

Requesting Debt Cards Post-Bankruptcy

Having actually gone over the distinctions in between secured and unprotected bank card, people who have actually gone through insolvency may currently consider the procedure of applying for bank card post-bankruptcy. Restoring credit rating after bankruptcy can be difficult, but obtaining a bank card is an important action in the direction of enhancing one's creditworthiness. When requesting bank card post-bankruptcy, it is essential to be tactical and careful in picking the best alternatives.

In addition, some people may qualify for certain unsecured credit rating cards especially made for those with a history of insolvency. These cards may have greater charges or rates of interest, yet they can still give a chance to restore credit rating when utilized properly. Before obtaining any charge card post-bankruptcy, it is advisable to assess the terms and problems meticulously to recognize the charges, rate of interest, and credit-building potential.

Credit-Boosting Approaches for Bankrupts

For people looking to improve their credit scores after bankruptcy, one essential strategy is to obtain a secured credit card. Protected cards call for a cash money deposit that offers as collateral, enabling individuals to show liable credit report usage and repayment behavior.

Another strategy involves ending up being an authorized user on someone else's charge card account. This allows people to piggyback off the key account holder's positive debt background, possibly boosting their own credit history. However, it is important to ensure that the primary account holder maintains great credit score habits to make the most of the advantages of this technique.

Furthermore, continually keeping track of credit score reports for inaccuracies and contesting any kind of mistakes can additionally help in boosting credit history. By staying aggressive and disciplined in their credit report management, individuals can gradually enhance their credit reliability even after experiencing personal bankruptcy.

Final Thought

Finally, released bankrupts can obtain bank card by meeting qualification requirements, reconstructing credit report, comprehending the difference in between protected and unprotected cards, and applying strategically. By following credit-boosting methods, such as keeping and making timely repayments credit score application reduced, insolvent individuals can slowly improve their creditworthiness and accessibility to credit report cards. It is this content essential for discharged bankrupts to be persistent and mindful in their monetary habits to successfully navigate the process of getting credit history cards after personal bankruptcy.

Comprehending the rigorous debt card eligibility criteria is important for people looking for to acquire credit report cards after insolvency. While secured cards provide a course to boosting credit report, unsecured cards provide more versatility but might be tougher to acquire for those with a struggling credit rating background.

In final thought, discharged bankrupts can obtain credit score cards by fulfilling eligibility standards, restoring credit, understanding the difference between secured and unprotected cards, and applying click to read more purposefully.

Report this page